Quick Answer

To get mortgage pre-approval in BC’s spring market, gather your income, asset, debt, and identification documents, then apply with a lender or mortgage broker for a written pre-approval letter. This confirms your maximum purchase price, interest rate hold, and strengthens your offer in a competitive market.

Why is mortgage pre-approval essential in BC’s spring market?

Mortgage pre-approval is essential in BC’s spring market because it shows sellers you’re serious and ready to buy. With multiple offers common in cities like Vancouver and Surrey, a pre-approval letter gives you a negotiating edge and speeds up the buying process. Sellers often favour offers from pre-approved buyers, and it helps you avoid the disappointment of falling in love with homes that are out of your price range. In regions like Victoria and Burnaby, where spring listings move quickly, pre-approval can be the difference between winning and losing a home.

What documents do you need for mortgage pre-approval in BC?

To get mortgage pre-approval in BC, you’ll typically need proof of income, employment letters or recent pay stubs, tax documents, a list of assets and debts, government ID, and recent bank statements. Lenders use these to assess your creditworthiness and determine your maximum mortgage amount. If you’re self-employed, expect to provide at least two years of tax returns and Notices of Assessment. Having these documents ready before you contact a lender or mortgage broker will streamline the process during the busy spring season.

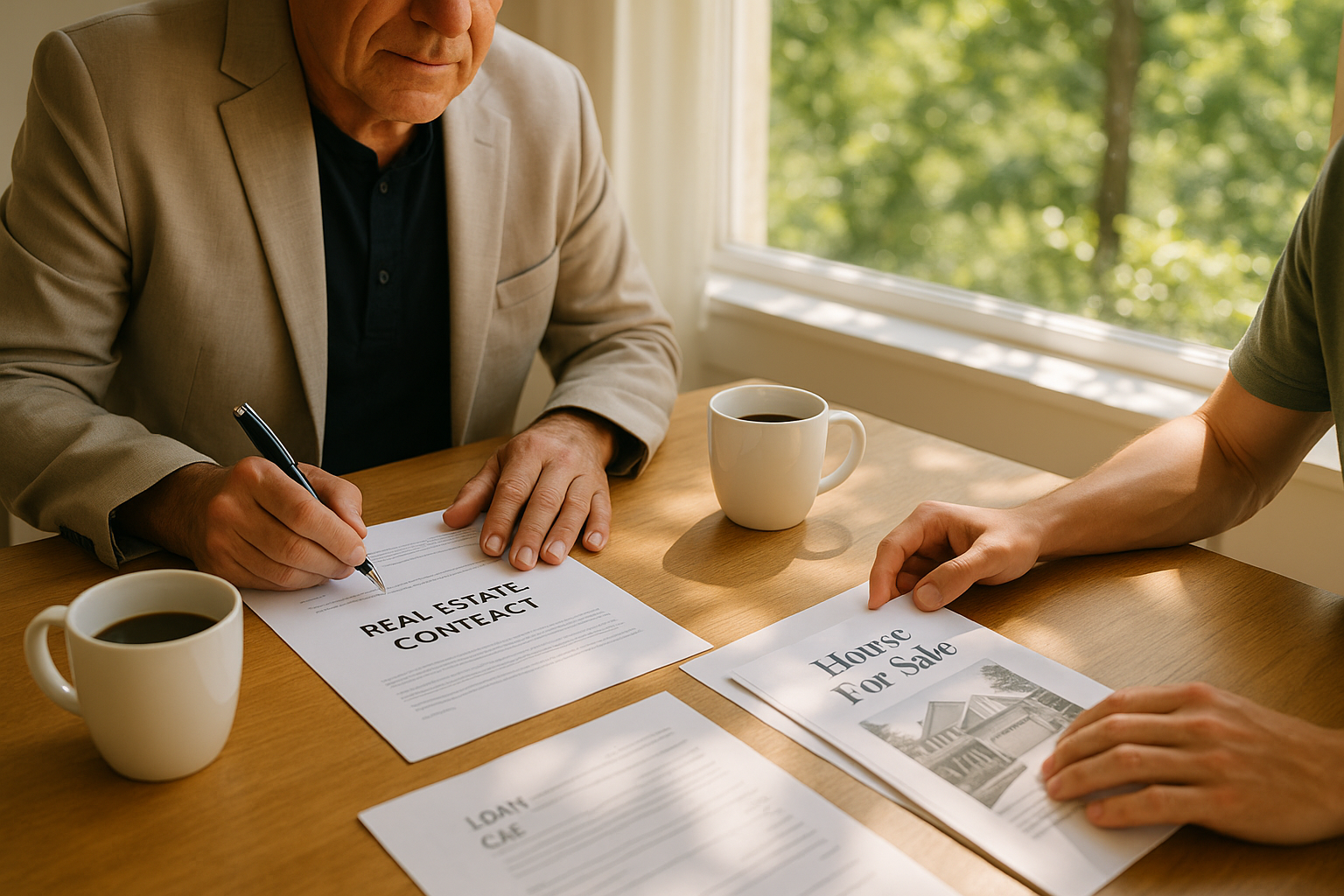

How does the pre-approval process work with BC lenders and brokers?

The pre-approval process in BC starts when you submit your documents to a bank, credit union, or mortgage broker. They’ll run a credit check, calculate your debt service ratios, and evaluate your eligibility under current Canadian mortgage rules. Within a few days, you’ll receive a pre-approval letter stating your maximum purchase price and a locked-in rate (usually for 90–120 days). Mortgage brokers can shop your application to multiple lenders, sometimes finding better rates or products than big banks, which is valuable in competitive spring markets like Vancouver or Victoria.

What mistakes should buyers avoid when seeking pre-approval in spring?

Buyers should avoid common mistakes like assuming pre-qualification is the same as pre-approval, making big purchases or switching jobs before closing, or omitting debts from their application. Pre-qualification is only an estimate and won’t carry weight with sellers. Also, avoid any major changes to your credit or finances during the buying process, as lenders may re-check your status before final approval. In fast-moving markets like Surrey or Richmond, even a small error can cause financing issues or missed opportunities.

What’s the next step after getting pre-approved for a mortgage in BC?

After getting pre-approved, your next step is to start viewing homes within your budget and prepare for quick offers. In spring, many buyers encounter competitive situations or tight subject removal periods, so having your mortgage pre-approval ready enables you to act fast. Don’t forget other due diligence—especially reviewing strata or property documents. Tools like SearchStrata can help you analyze strata packages so you can make confident, informed offers on condos or townhomes.

Frequently Asked Questions

How long does mortgage pre-approval last in BC?

Mortgage pre-approval in BC typically lasts 90 to 120 days, giving you a window to shop for a home while locking in your interest rate.

Does pre-approval guarantee I’ll get the mortgage?

Pre-approval does not guarantee final mortgage approval; your lender will reassess your finances and the property details during the full approval process.

Is a mortgage broker better than a bank for pre-approval in BC?

A mortgage broker can offer more options by shopping your application to multiple lenders, while banks only provide their own products. It depends on your financial situation and preferences.

Can I get pre-approved if I’m self-employed in BC?

Yes, self-employed BC buyers can get pre-approved, but you’ll need to provide more documentation, such as at least two years of tax returns and recent Notices of Assessment.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a basic estimate of how much you might borrow, while pre-approval involves a thorough review of your finances and results in a formal letter from a lender.

Conclusion

Mortgage pre-approval is your ticket to moving quickly and confidently in BC’s busy spring market. By preparing your documents, understanding lender expectations, and avoiding common mistakes, you’ll be ready to compete. When you find a property you love, make sure to review the strata or property documents thoroughly—SearchStrata can make this part of the process faster and simpler.